Long ass read..but informative..

CENTRAL BANKING

Bank Fees…The Good, The Bad and the Very Ugly

March 6, 2017 Jwala Rambarran

Do you know how much you paid your bank last year for the convenience of using its services? Some of us may have an idea how much our bank’s services cost, but do we add it all up at the end of the year?

Many Trinis believe the fees they pay commercial banks for their services are unfair, onerous and eat into their hard-earned money. They complain about poor customer service, shortage of staff at the counters, and lack of basic amenities particularly for the elderly when they have to stand in long lines for lengthy periods.

Any imposition of new or increased bank fees almost always invokes howls of protest, especially when banks announce multi-million dollar profits. It’s the epitome of big business versus the small working class man or woman.

There has been growing public resentment towards banks over the fees they charge for their services. That resentment clearly isn’t dying down.

Bank fees have become so controversial the issue recently came under Parliamentary scrutiny with the Central Bank Governor appearing before the Joint Select Committee (JSC) on Finance and Legal Affairs which held a public hearing on the matter.

I found the questions from the JSC members were probing, relevant and very much in the public’s interest. JSC members should be commended for the considerable effort they had obviously put into their preparation for the session. It was a good example of how the Parliament could be used effectively to ventilate a matter of widespread public concern.

It’s disappointing, however, that the Central Bank Governor, as head of our national institution responsible for regulating banks, never once provided a clear answer to any of the questions posed to him by JSC members.

When the Governor danced around and avoided answering their questions, each JSC member pressed him further, as they quite rightly expected a Central Bank Governor to be competent and articulate enough to provide coherent responses on any economic matter. This is where it got even more tragic and disturbing.

Asked, in relation to bank service charges, which bank is the most dominant, the Governor responded that due to the secrecy provisions of the Central Bank Act and observing “good business practice” he could not answer this question.

The JSC member who asked this question, Government Senator Michael Coppin, later pointed out to the Governor that the information on bank fees which he refused to divulge is actually available on the Central Bank’s own website.

So why then would the Central Bank Governor not make more of an effort to answer basic and valid questions about the banking industry in our country? The answer is simple; it has nothing to do with confidentiality, but with courage.

As the prime regulator, the Governor needs to be reminded he’s in the business of central banking, not commercial banking. He’s duty bound under Section 3 (3) of the Central Bank Act to promote such monetary, credit and exchange conditions as are most favourable to the development of the economy of Trinidad and Tobago.

So naming the commercial bank that dominates bank fees wouldn’t hurt the regulator’s business, as his business is to protect the country’s economic interests. When it’s in the public’s interest to know, the Central Bank Governor must have the courage to give the country the information it is desperately asking for and not cower.

(I strongly recommend you look at the Central Bank Governor’s appearance before the JSC, it’s on YouTube/Parliament Channel in case I’m accused of being biased. Judge for yourself. Are you left feeling this person can be entrusted to seek your interest?)

So in the interest of better informing and educating the public, I have analyzed data from three public sources to provide you with the good, the bad and the very ugly sides of bank fees in Trinidad and Tobago. There are no confidentiality issues here and as the former Central Bank Governor I am not in breach of the confidentiality agreement I signed upon my appointment.

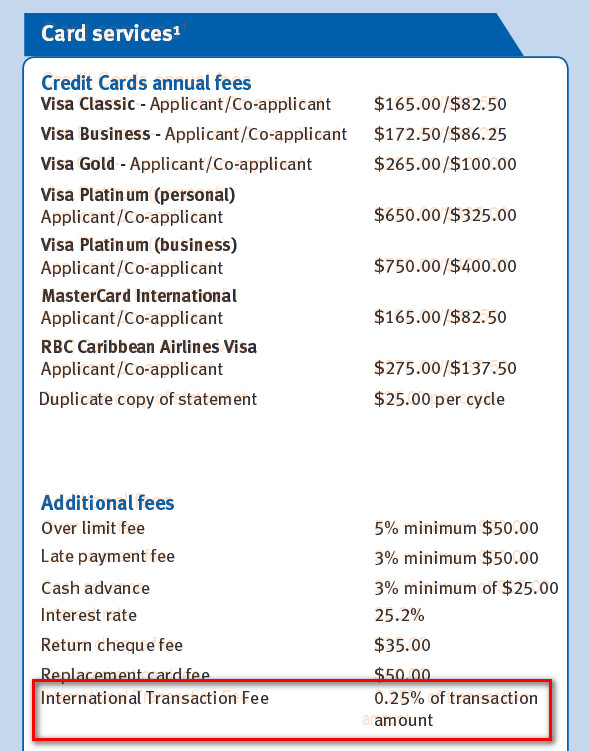

The first data source is the Central Bank’s “Comparative Schedule of Commercial Banks’ Fees and Charges”. The Schedule, based on work I initiated when I was Central Bank Governor, provides comparative data on key fees and charges for all eight commercial banks operating in Trinidad and Tobago as at June 30th 2016. It covers six main service categories: savings accounts, chequing accounts, lending services, credit cards, electronic transactions and miscellaneous bank services.

This data was used to rank banks by the incidence of highest personal banking fees, to determine which banks offer the highest number of free services, and to gauge whether banks charge the same fee for the same service. The analysis covered seven of the eight banks in Trinidad and Tobago. Citibank is excluded because its corporate banking model is not relevant to the retail market.

A standard competition ranking strategy was used to rank the banks, ordering the data from one to seven, with a score of one assigned to the bank with the lowest fee per retail service item and a score of seven to the bank with the highest fee per retail service item. This analysis was carried out for more than 50 service items and aggregated these across the six main service categories to arrive at an overall rank for each bank.

The second data source is the Central Bank’s “Operating Results of the Financial System”. The Operating Results provide data on the performance of the commercial banking system, including income, expenses, assets and profitability.

Finally, data from the Schedule and the Operating Results were supplemented with information publicly available on the websites of commercial banks.

It is important to bear in mind the difficulties in making meaningful comparisons of bank fees in Trinidad and Tobago with those elsewhere, especially in developed countries like the United States, Canada and the United Kingdom. Differences in regulation, economies of scale and cost structures can all affect the fee a bank charges its customer.

Here then are 5 major findings on bank fees and service charges which every Trinidadian including the Central Bank Governor should know:

Bank Fees and Service Charges are the Largest Source of “Fee Income”

Commercial banks carry huge overheads in order to meet the needs and conveniences of their customers. In Trinidad and Tobago, the eight banks deploy a network of 135 branches and around 7,500 staff using highly specialized equipment and technology, ATMs and even security to meet the needs of their customers with 1.7 million deposit accounts and over half a million loan accounts. These costs have to be met from banks’ income.

About a decade ago, banks used earnings derived from their main revenue stream, interest income, to meet their overhead costs. Interest income essentially reflects the spread between the interest rates charged by banks on loans to borrowers and interest rates paid by banks to depositors. Bank fees and service charges were moderate.

Today, very low interest rates and weak loan demand have put significant pressure on interest income while leaving banks with still high operating costs to meet the needs and convenience of their customers. In these circumstances, banks have turned to income from non-interest sources, especially fee income and foreign exchange trading, to support their operations and profits.

Service charges now comprise the single largest source of fee income for commercial banks in Trinidad and Tobago. In 2015, banks earned $835 million in service fees, or about 70% of their total fee income.

A decade ago, banks collected $330 million in service charges which represented just over half of their total fee income.

Service fees now help banks cover 20% of the heavy overheads they incur to meet the needs of their customers and contributed to keeping banks’ profitability ratios stable over the last five years.

2. Scotiabank Ranks No.1 in Highest Bank Fees

Scotiabank ranks No.1 in terms of highest personal banking fees. In fact, Scotiabank has the greatest incidence of highest bank fees across all six main service categories: personal savings accounts, personal chequing accounts, lending services (installment loans and residential mortgages), credit cards, electronic transactions, and miscellaneous bank services.

Scotiabank requires its customers to maintain a minimum balance of $1,000 per month in their personal savings account, compared to the average industry balance of $100 per month. However, Scotiabank will waive its $10 maintenance fee once this monthly balance is kept.

If you make a deposit or withdrawal at any teller in Scotiabank’s branches, you pay a fee of $7 per transaction, the highest in the banking industry. At FCB, JMMB Bank, RBC Royal Bank and RBL, in-branch deposit/withdrawal transactions are free at the teller. These transactions attract a fee of $1 at Bank of Baroda and FCIB.

In the area of lending Scotiabank significantly surpasses other banks, with six of the highest lending fees on installment loans and residential mortgages.

Applying for an installment loan of less than $33,000 at Scotiabank, you pay a minimum application fee of $500; if the loan is greater than $33,000 your application fee doubles to a minimum of $1,000. At FCB and RBL, your loan application is free, while at Bank of Baroda there’s a minimum charge of $125.

Once Scotiabank decides to grant you a residential mortgage, you must pay an acceptance/commitment fee of 1.5% of the total mortgage amount plus an undisclosed inspection fee. At FCIB, RBC Royal Bank and RBL, the acceptance/commitment fee is set at 1% of the loan amount.

If you decide to refinance your mortgage, then you must pay Scotiabank a refinancing fee of $500 plus a commitment fee on the additional funds advanced. At RBL, there is no charge for refinancing your mortgage, while at Bank of Baroda and FCIB the refinancing fee is $250, half that charged by Scotiabank.

If you want to repay part of your mortgage with Scotiabank and bring down the annual mortgage payments, Scotiabank will charge you a prepayment fee at 180 days’ interest for the amount over your annual entitlement. At FCB and RBL there’s no charge for mortgage prepayments, while at RBC Royal Bank the prepayment fee is half that of Scotiabank, attracting 90 days’ interest.

Have you come into some extra money and want to pay off the full outstanding balance on your mortgage, then you must pay Scotiabank an early settlement fee of 180 days’ interest. At RBL, there is no charge for early settlement of your mortgage. At RBC Royal Bank, the early settlement fee is 90 days’ interest, half that charged by Scotiabank.

Scotiabank also has seven of the highest fees on electronic transactions even though banks have been encouraging customers to move out of their expensive banking halls and use more technology-driven services such as ATMs and internet and telephone banking.

Using your Scotiabank debit card to conduct electronic transactions, outside of the LINX network, can add up quickly, particularly if you use your debit card for multiple transactions throughout the month.

If you use your Scotiabank debit card to do an enquiry at a Scotiabank ATM, it costs you $1 per transaction, depending on the nature of your account. This ATM enquiry fee is free at all other banks.

If you use your Scotiabank debit card to withdraw cash at a Scotiabank ATM, it attracts a fee of $2 per transaction. Bank of Baroda, FCIB, JMMB Bank and RBC Royal Bank do not charge their customers to withdraw cash at their own branch ATMs. RBL charges its customers a fee of $0.75 per transaction to withdraw cash from its ATM network and at FCB the ATM withdrawal fee is $0.85 for its customers.

If for some reason your cash withdrawal transaction is declined at your Scotiabank ATM, you must pay a $1 ATM withdrawal decline fee. Bank of Baroda, FCIB, FCB and JMMB Bank do not charge their customers for cash withdrawals declined within their own branch ATMs. At RBC Royal Bank, its customers pay an ATM cash withdrawal decline fee of $0.50 per transaction and at RBL this fee is $0.75 for its customers.

Scotiabank is the only bank that charges its customers to use their Scotiabank credit cards to pay their TSTT, WASA or TTEC bills online. Using either internet or telephone banking to pay a utility bill attracts a minimum utility payment fee of $25 per transaction from Scotiabank.

Need to wire transfer funds to the United States? Well that’s going to cost you $75 per transaction at Scotiabank and this wire transfer fee (outgoing) could increase further if Scotiabank decides to add on beneficiary charges. Wire transfer fees (outgoing) typically average $65 per transaction at most other banks.

Need a statement from Scotiabank to take to the US Embassy? That’s going to cost you $37. The cost of a similar embassy statement ranges from $20 at FCIB to $30 at both JMMB Bank and RBC Royal Bank.

Do you want a safety deposit box to keep your valuable documents and jewelry? Well that service costs a minimum of $350 per year at Scotiabank. Rental of a safety deposit box ranges from a minimum of $74.75 per year at JMMB Bank to $250 per year at both RBC Royal Bank and RBL.

After Scotiabank, RBC Royal Bank ranks second in terms of highest personal banking fees. Except for credit card fees where it ranks lowest, RBC Royal Bank is No.2 in terms of highest fees in the other five main service categories: personal savings accounts, personal chequing accounts, lending services (installment loans and residential mortgages), electronic transactions and miscellaneous bank services.

Even after March 27, 2017 when it will introduce several new fees and increase some of its existing fees, RBC Royal Bank will maintain its second-place highest fee ranking.

RBL ranks third in terms of highest bank fees, especially on savings accounts, credit cards, and electronic transactions.

FCB is the median bank with average bank fees, ranking fourth out of the seven banks.

JMMB Bank follows as the fifth ranked bank when it comes to bank fees, while Bank of Baroda ranks sixth.

First Caribbean International Bank (FCIB) has the lowest incidence of personal banking fees, especially on chequing accounts, electronic transactions, and miscellaneous bank services.

3. RBL Offers the Highest Number of Free Banking Services, Scotiabank the Least

Banks do offer free personal banking services to their customers. Most banks do not charge their customers for services such as in-branch deposit transactions, routine credit card statements, ATM enquiries/withdrawals using either their own ATMs or the LINX network, first issue of a debit card, use of internet/telephone banking to pay utility bills, and settlement of incoming high value transactions at $500,000 and over.

RBL offers the highest number of free personal banking services, providing 22 service items free of charge. Apart from the service items which most banks provide free, RBL leads all other banks in not charging its customers for nearly all its lending services.

If you apply for either an installment loan or a residential mortgage at RBL, you do not pay any application fee or credit report fee. Once your installment loan or residential mortgage is granted and at some point you wish to either refinance or make an early settlement or prepayment, RBL does not charge for these services.

Scotiabank offers the least number of free personal banking services, providing only five service items free of charge.

A Scotiabank retail customer does not pay for a routine credit card statement, first issue of a Scotiabank debit card, use of internet/telephone banking and to pay a utility bill online (except with a credit card), and to settle a high value transaction of at least $500,000. However, these five free services which Scotiabank offers are also provided for free by nearly all other banks.

4. Banks Operate in an Oligopoly and Do Not Competitively Set Fees

Testifying before the Joint Select Committee, the Central Bank Governor said banks are competitive in Trinidad and Tobago and, by extension, their fees and service charges reflect the cost of providing their banking services. That assertion is completely false.

I fully agree with JSC member, Housing Minister Randall Mitchell, who not only disagreed with the Governor but was forceful in his assessment that banking is an oligopoly in Trinidad and Tobago where a handful of banks dominate the market.

Data from various annual reports of the four largest banks – RBL, FCB, RBC Royal Bank and Scotiabank – show their market dominance. They collectively control 90% of total banking sector assets. Two banks – RBL and FCB – together control 75% of total deposits and 70% of total loans. One bank – RBL – controls 25% of the foreign exchange market.

This very high degree of bank concentration in Trinidad and Tobago suggests the market for financial services is not as competitive as the Central Bank Governor believes it to be and might be contributing to retail bank fees that are not “fair and reasonable”.

So while in theory customers are free to switch from one bank to another, in reality this is not truly practical. High transaction costs of changing banks – loans tied to an existing bank and burdensome paperwork to move accounts – deter most customers from switching banks.

Banks operating in an oligopoly market structure usually do not compete on the basis of price (fees) but engage in extensive non-price forms of competition, especially quality of service.

Perhaps this explains why the four largest banks in Trinidad and Tobago show little variation in their fees for the same personal banking service in 24 service offerings. The near uniformity in their bank fees is particularly striking in the loan market and the credit card market.

Collusion has often been put forward as a reason for weak bank competition in Trinidad and Tobago. “Price fixing” is a matter which keenly attracted the interest of JSC member Coppin. The main avenue for banks to collude on price fixing is tacit, that is, banks have some understandings about fees and service charges.

While the publicly available evidence is not strong enough to categorically state the four largest banks collude to fix fees, the observed pricing behavior does raise suspicions about the potential for collusion in some parts of the personal banking market. The JSC on Finance and Legal Affairs should give further consideration to the possibility that the four largest banks might be abusing their dominant market position.

5. Central Bank Has Power to Influence Bank Fees

Responding to a question from JSC member Minister Randall Mitchell on the Central Bank’s ability to influence bank fees, the Governor citing Section 44A of the Central Bank Act figuratively threw his hands up into the air and surrendered, lamenting that the Central Bank has no regulatory powers to deal specifically with bank fees. That is not true.

Section 44A of the Central Bank Act does indeed restrict the Central Bank’s power to regulate fees and charges on credit facilities and on loans and advances, not fees and service charges on credit cards, ATM transactions and bank statements.

But Section 44A of the Central Bank Act is irrelevant since it applies to the pre-1993 period of “financial repression’, when the Central Bank imposed controls on interest rates and consumer loans at commercial banks.

Yes, there was a time almost 25 years ago, when the Central Bank told banks what was the maximum interest rate they could charge on loans, eliminated the minimum down payment requirement, and extended loan repayment periods. The Central Bank also placed a ceiling on the maximum each bank could lend to finance consumer durables.

With financial liberalization taking place after 1993 these instruments of direct monetary management were gradually scrapped and the Central Bank adopted a new monetary policy framework, which is in operation today. In that new framework, the Central Bank uses a policy interest rate – the Repo rate – as its main operating instrument to influence interest rates in the banking system.

In an oligopolistic banking structure with significant bank concentration, however, the Repo rate cannot influence bank fees so the Central Bank Governor has resorted to moral suasion, simply talking and writing to the banks about bank fees and hoping they listen and respond favorably. Like the Repo rate, moral suasion has limited power in an oligopolistic banking market.

Does the Central Bank have any powers left to influence bank fees? Yes, of course.

That power resides in Section 3 (3) (c) of the Central Bank Act, which gives the Central Bank the power to… “maintain, influence and regulate the volume and conditions of supply of credit and currency in the best interest of the economic life of Trinidad and Tobago.”

That power also resides in Section 3 (3) (d) of the Central Bank Act, which gives the Central Bank the power to… “encourage expansion in the general level of production, trade and employment.”

The Central Bank Governor needs a refresher course on the broad development mandate of the Central Bank enshrined in Section 3 of the Central Bank Act which gives him the power to act in the best economic interests of the country.

He also needs to be reminded about “contestability”, the most influential economic theory on competition, which not only gives life to the legislative provisions of Section 3 but gives the Central Bank the ability to influence bank fees.

Contestability refers to the ease with which new firms can enter or exit a market. It’s the factor that most influences the degree of competition in a given market. In other words, incumbent banks will behave in a competitive manner so long as the Central Bank allows new banks to enter and compete for market share. But not just any new bank.

In 2000, the Centre for Latin American Monetary Studies (CEMLA) published in its well-respected, international journal “Money Affairs” the only known public study on bank competition and contestability in Trinidad and Tobago.

The study found that Trinidad and Tobago has a partially contestable banking market, and the entry of at least two more medium-sized banks would bring greater competition, reduce interest rate spreads and bank fees, and provide a broader range of financial services.

Since then, the Central Bank allowed two banks – JMMB Bank (formerly Inter-Commercial Bank) and Bank of Baroda – to enter the market, but their small scale of operations remains insufficient to trigger any significant degree of competitiveness in the banking sector. In fact, JMMB Bank and Bank of Baroda are the two smallest banks operating in Trinidad and Tobago.

So it’s strange to hear the Governor state that Trinidad and Tobago is overbanked and to suggest that’s why the Central Bank would not grant any more banking licenses to prospective entrants.

Putting it simply, the Governor asserted (without citing any evidence to support his claim) there’s just not enough banking business in the country to sustain the existing eight banks, much less encourage additional banks to come in and set up shop.

Again, nothing could be further from the truth. Key sectors of the Trinidad and Tobago economy are actually under-funded, despite the immense potential for banks to grow more business, gain more interest income and reduce their reliance on bank fees.

Government has identified several industries necessary for successful economic diversification. These industries are agriculture and agro-processing, maritime services, fish and fish processing, aviation services, the creative industries, and software design and applications. Our Canadian-dominated banking model does not actively fund these industries.

The small and medium enterprises (SMEs) sector is another under-funded area. Almost 18,000 SMEs depend on banks to finance their business but are increasingly demanding more customized banking products, not just the one-size-fits-all product basket. Banks offering new digital finance products such as mobile money and e-commerce can play a key role in meeting the unfulfilled needs of SMEs.

Government intends to encourage the New Development Bank (the world’s newest multilateral development bank owned by the BRIC countries) and two state-owned Chinese banks to establish branches in the Trinidad and Tobago International Financial Centre (TTIFC). These banks would then fund projects throughout Latin America and the Caribbean.

This expansion of the TTIFC should generate a significant increase in demand for commercial banks to provide back-office, banking and capital market activities related to the South-South trade and investment flows that will be originating from Trinidad and Tobago as these new entities set up shop.

Under-funded economic sectors, SMEs and South-South banking activities offer ample opportunities for new or existing banks to grow their loan portfolios, narrow interest rate spreads, and reduce bank fees and service charges.

Trinidad and Tobago is underbanked!!!

The Road Ahead

Bank fees thrive in the darkness of ignorance and the fine print of monthly bank statements. Banks ambiguity about the manner in which they communicate their fees and service charges worsens the situation and further adds to the public’s growing dislike of the local banking giants.

What then might be potential solutions to dealing with the contentious issue of bank fees? I believe action is needed by three main players – the Bankers Association of Trinidad and Tobago (BATT), the Office of Financial Services Ombudsman (OFSO), and the Central Bank.

First, BATT should develop a standardized terminology for the most commonly used personal banking services, making full disclosure of all relevant and material information. It can take a page or two from UK banks which are among the most transparent banks in the world in their presentation of information about charges for their services.

This standard language would result in an easy to read schedule of bank fees and service charges for each bank and take the mystery out of how much banks charge for their various services. But simplicity is not enough. Comparability is necessary.

All commercial banks should prominently display a comparative schedule of bank fees and service charges in their banking halls and on their websites and mail them out with the same vigor as they do for promotional offers. This would allow customers to better compare bank fees and service charges and to make more informed decisions when it comes to opening or switching bank accounts.

Transparency is next. Each month, banks should inform their customers through their bank statements of the total they paid in bank fees, not bury the fees within the minutiae of account activity history. Banks should also provide this information on an annual basis to their customers.

And above all, communications. BATT should mount a national communications campaign around bank fees, and do all it can to reach its customers down to the elderly like the mother of JSC member Agriculture Minister Clarence Rambharat, who cited his mother from Rio Claro (my place of birth) during the public hearing as an example of one of those bank customers who will not use internet banking but needs in-person interaction and explanations.

Second, the Office of the Financial Services Ombudsman (OFSO) must be given legislative authority to strengthen the regime of financial consumer protection. The OSFO was established to give hundreds of thousands of bank customers a voice when they have complaints which they feel cannot be resolved by their banks.

Unfortunately, the voluntary nature of the OSFO limits its jurisdiction to a narrow list of complaints to which banks have agreed. Bank fees are not on that agreed list, even though many of the banking complaints the OFSO receives relate to bank fees and pricing of bank products and services.

When I was Central Bank Governor, I started the process of upgrading the regime of financial consumer protection. Key to that upgrade is changing the voluntary nature of the OFSO to one established by law. A Proposed Policy Document, based on the UK Financial Ombudsman Service, was developed to inform draft legislation relating to the creation of a statutory Financial Services Ombudsman in Trinidad and Tobago

Unfortunately, this process appears to have stalled. It’s imperative it restarts to empower bank customers with a stronger voice when it comes to addressing their complaints about bank fees and service charges.

Finally, the Central Bank must promote bank competition within an appropriate framework of prudential regulation. Local banks have become comfortable, perhaps too comfortable with the sight of long lines of customers winding around their banking halls. Yet these customers are the ones who are literally paying the price for banks’ easy come attitude.

Competition works well in banking when rival banks vigorously seek and woo one another’s customers with innovative products, lower fees and better service. This is more likely to be the case in Trinidad and Tobago if the Central Bank allows at least two more medium-sized (about $40 billion each in assets) non-Canadian banks to enter our financial market.

Until more competitive banking conditions take root, the Central Bank should issue prudential guidelines on bank fees and service charges. These prudential guidelines would give the Central Bank authority to evaluate whether existing or new fees are reasonable and fair in relation to the customer, and to approve, modify or reject such fees.

The Central Bank of Ireland, which is a mega-regulator similar to our Central Bank, provides the appropriate model we can look at for some inspiration on how to bring some fairness and balance to bank fees in Trinidad and Tobago.

The Irish regulatory framework for bank fees seeks to promote competition and improve consumer protection while enabling banks to price their service costs efficiently. It shows how competition and prudential regulation can coexist comfortably, ensuring a stable banking system that adequately serves small customers, businesses and the economy.

I believe the questions the members of the JSC on Finance and Legal Affairs posed on bank fees have finally been answered.

(Disclosure: Jwala Rambarran has been a customer of RBC Royal Bank for the past 30 years)